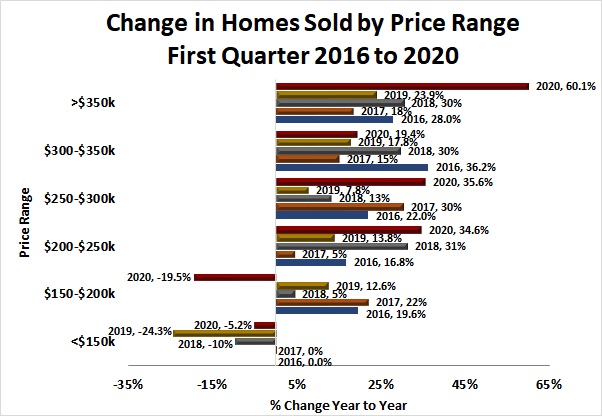

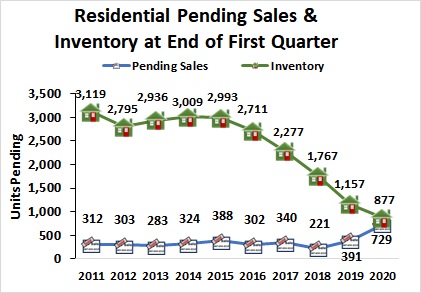

Homes Sold

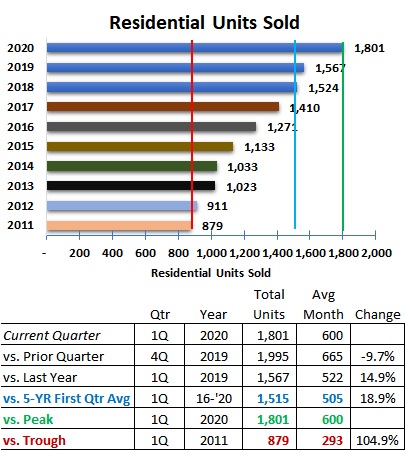

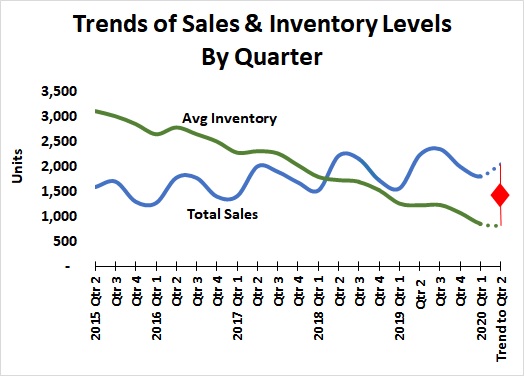

Sales continued at record levels in the first quarter 2020 but below the fourth quarter level of last year. The total units sold 1,801 this year is 14.9% above the 1,567 in the first quarter 2019 and more than twice the lowest first quarter total in 2011, which was a total of 879. See Figure 2.

The five-year average first quarter total sales increased to 1,515 which is 9.7% higher than the five-year first-quarter average of 1,381 in 2019.

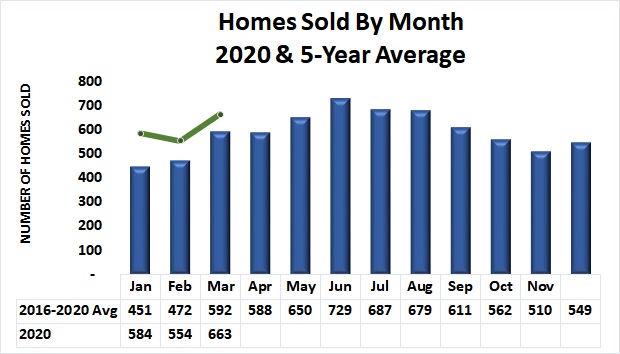

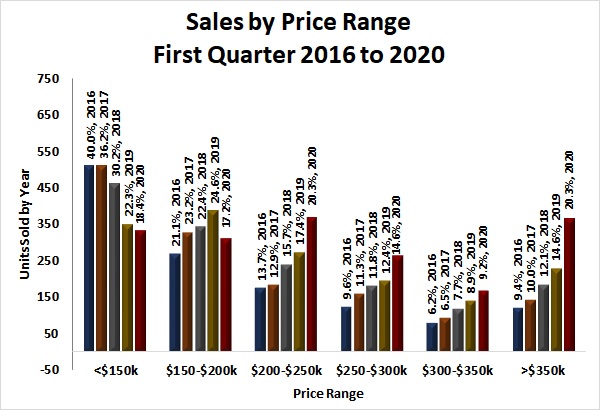

Homes Sold by Month

Comparing homes sold to the five-year monthly average shows that sales in 2020 sustained higher than normal levels from January through March. January’s actual sales of 584 was 29% above the five-year average January sales. February actual sales of 554 was 17% above the February average of 472. March sales (663) was 12% above average.