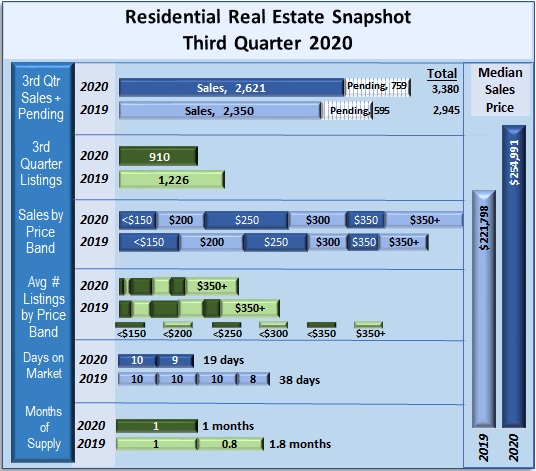

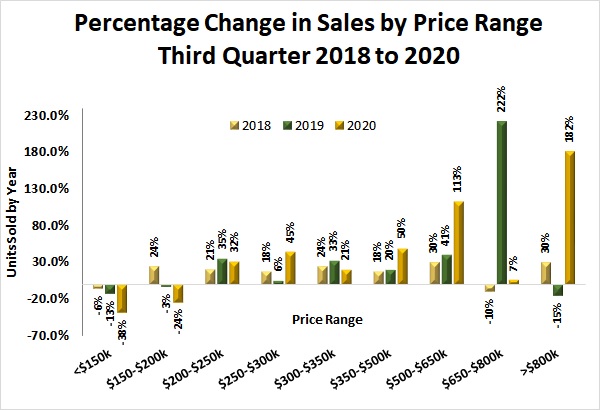

Sales Price Band: Less than $150,000 sales fell to 286 (-38%) sales compared to 461 in 2019

- $150,000-$200,000 sales fell to 375 (-24%) sales compared to 494 in 2019

- $200,000-$250,000 sales rose to 624 (32%) sales compared to 473 in 2019

- $250,000-$300,000 sales rose to 446 (45%) compared to 307 in 2019

- $300,000-$350,000 sales rose to 287 (21%) compared to 237 in 2019

- Over $350,000 sales rose to 603 (59%) compared to 378 in 2019

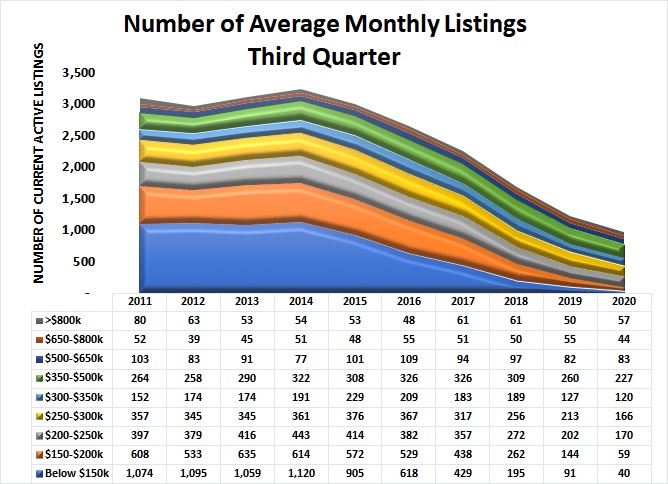

Inventory: – Less than $150,000 fell to 40 (-57%) homes vs. 91 in 2019

- $150,000-$200,000 fell to 59 (-59%) homes vs. 144 in 2019

- $200,000-$250,000 fell to 170 (-16% homes vs. 202 in 2019

- $250,000-$300,000 fell to 166 (-22%) homes vs. 213 in 2019

- $300,000-$350,000 fell to 120 (-5%) homes vs. 127 in 2019

- Over $350,000 fell to 411 (-8%) homes vs. 447 in 2019