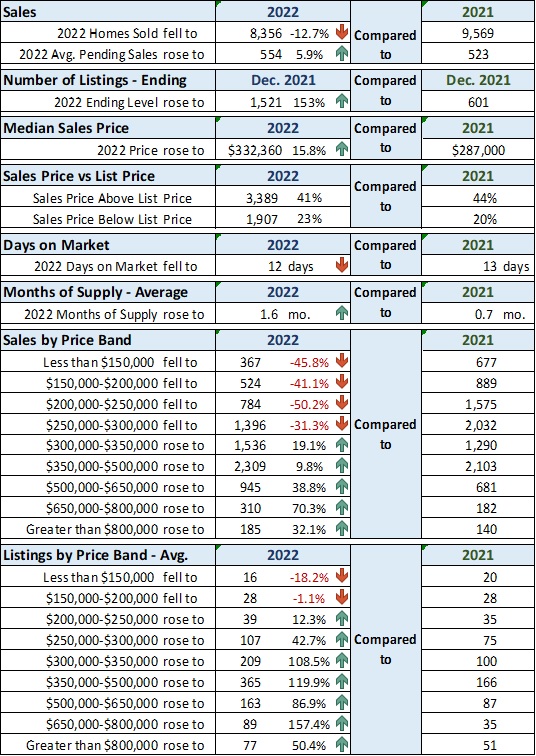

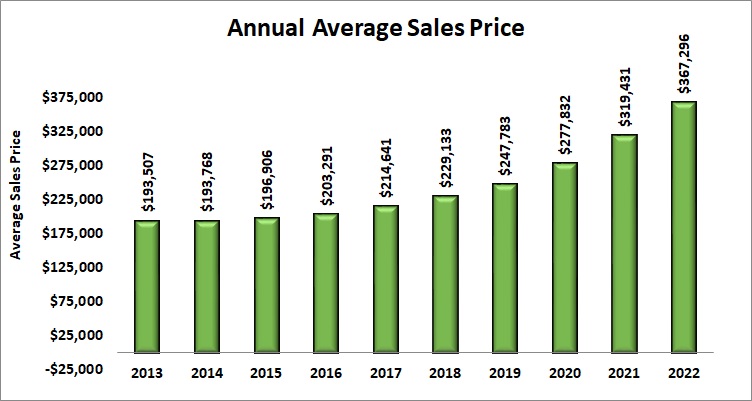

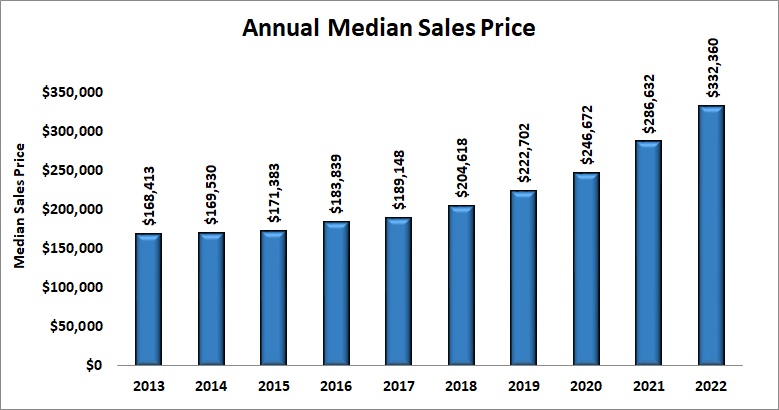

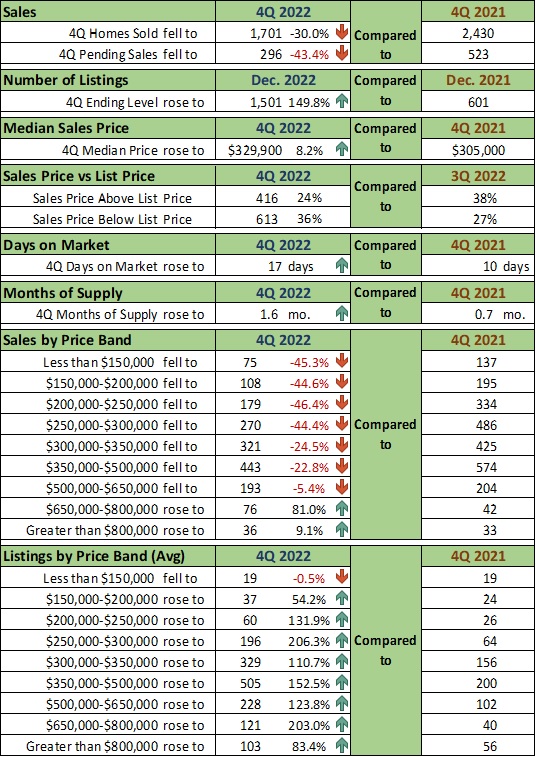

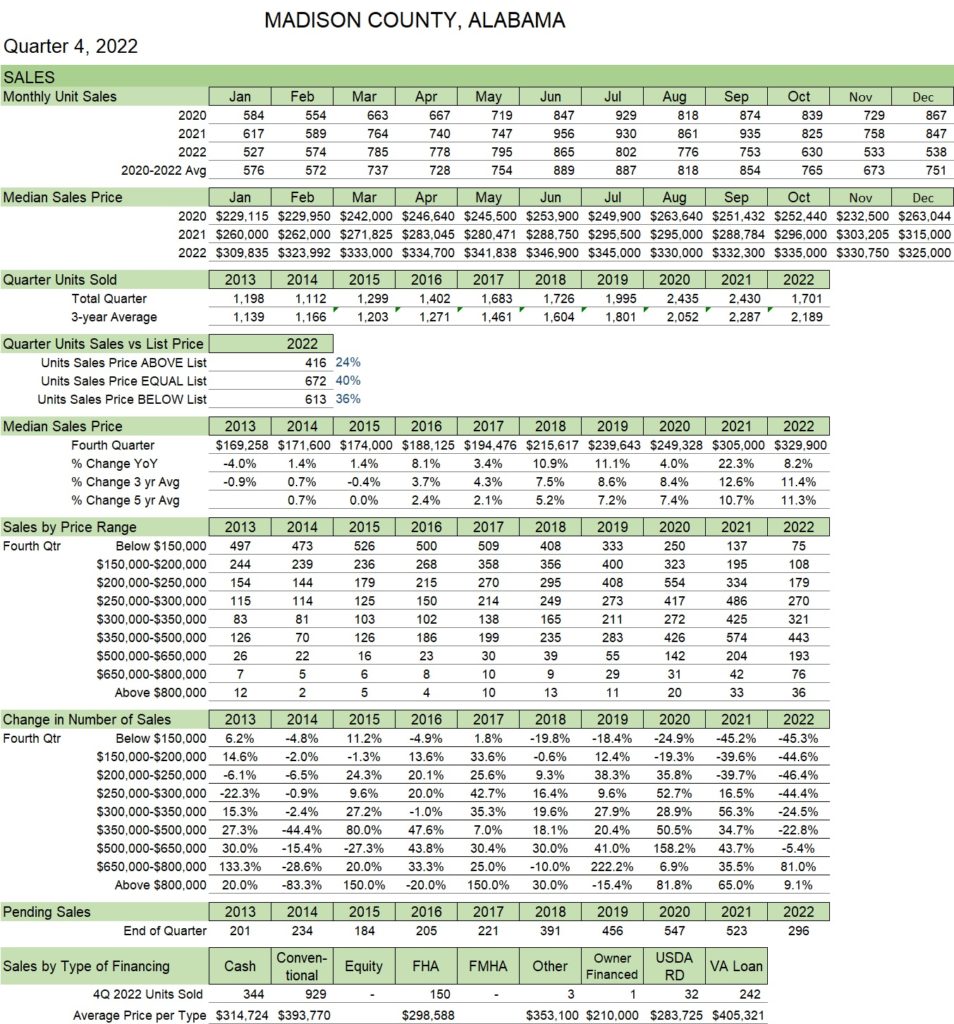

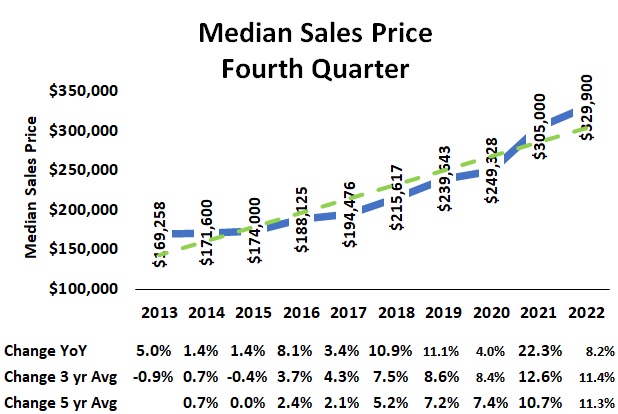

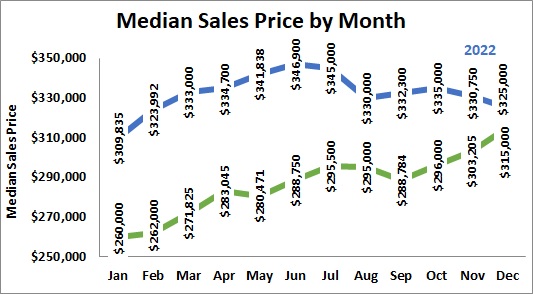

The median sales price of all homes sold grew during the first six months and retreated slightly resulting in an annual median of $332,360.

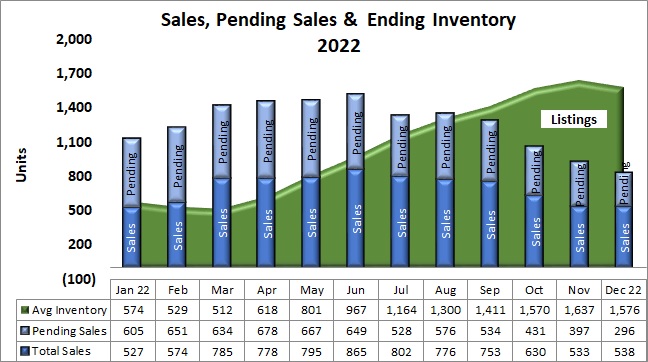

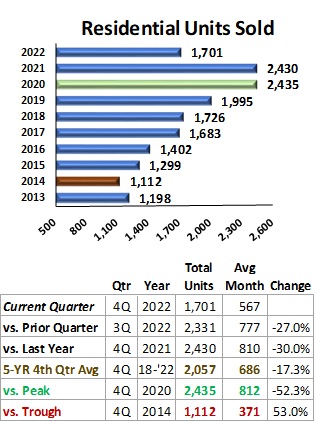

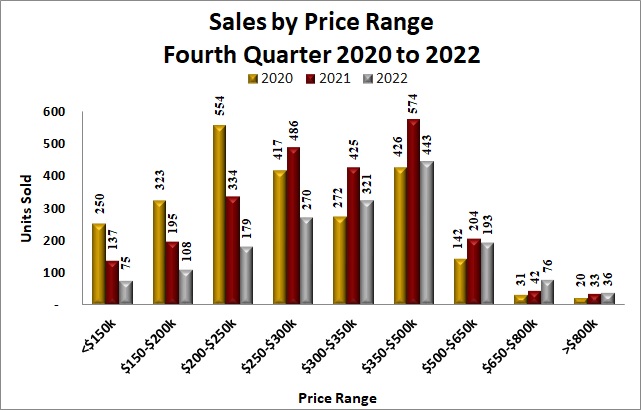

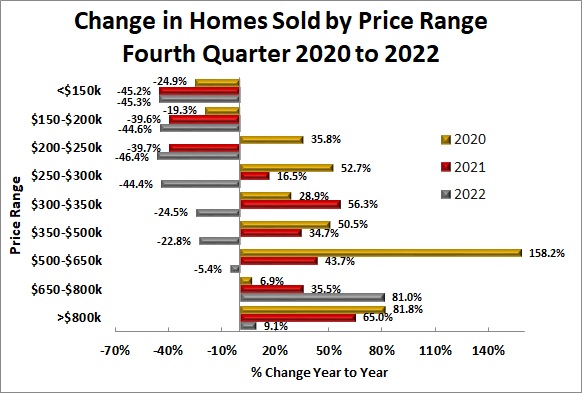

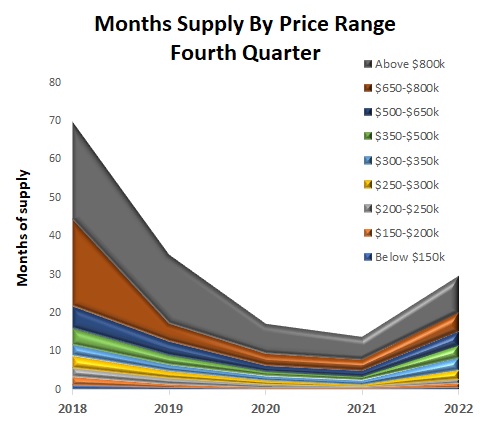

By price band, sales of homes priced below $300,000 fell. Number of homes sold rose in all price bands above $300,000. Sales of homes priced between $650,000 and $800,000 saw the largest percentage increase at 70%. The greatest number of homes sold (2,309) were priced between $350,000 and $500,000.

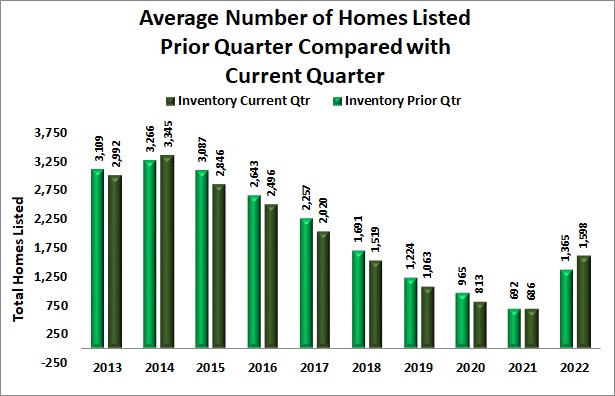

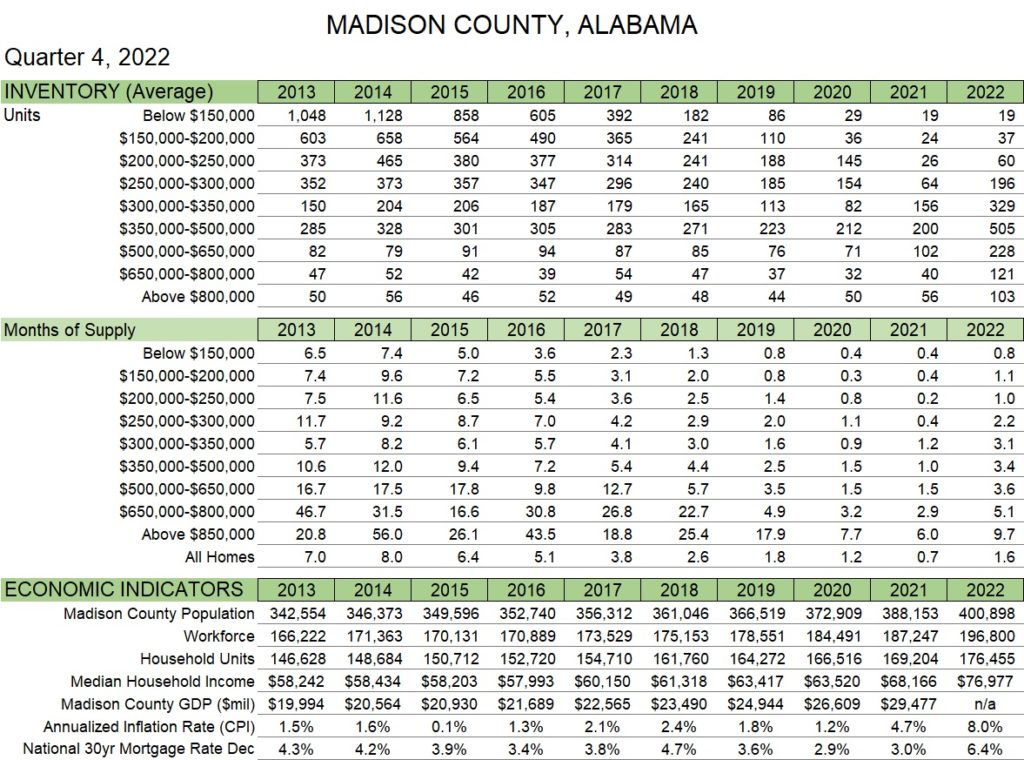

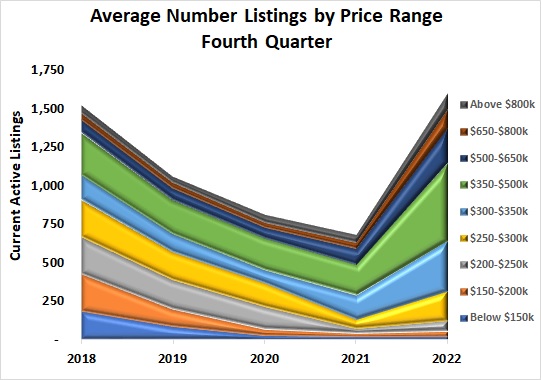

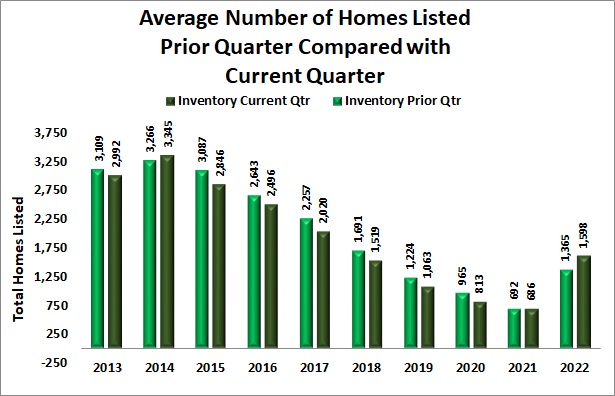

Listings of homes available for sale rose significantly in all price levels above $200,000. The largest average number of homes listed for the year was for homes priced between $350,000 – $500,000. See Table 1.