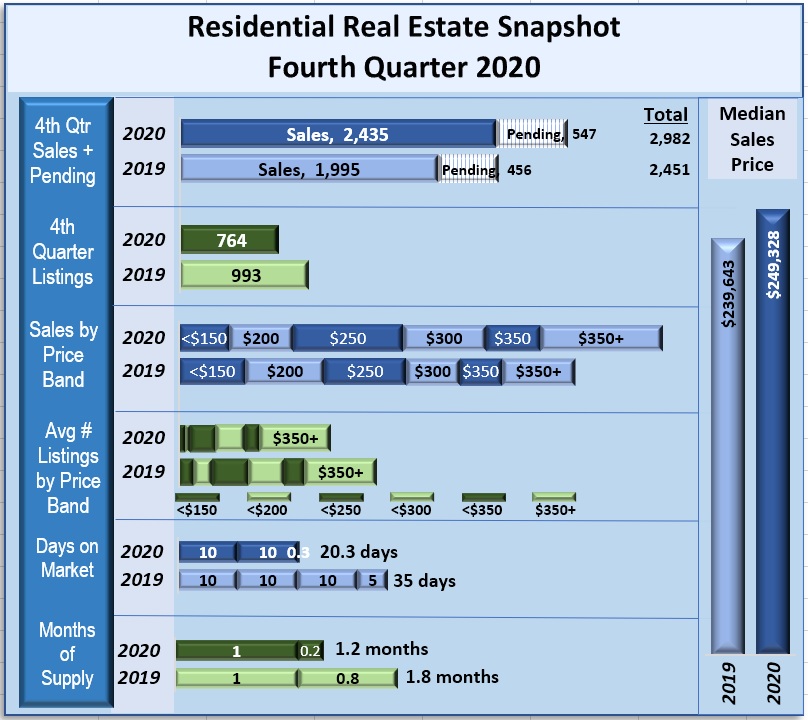

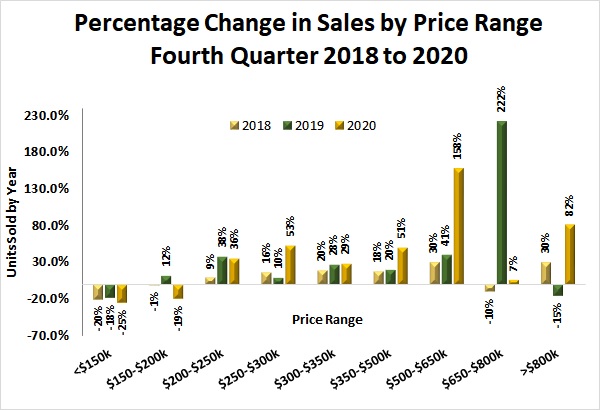

Sales Price Band: Less than $150,000 sales fell to 286 (-38%) sales compared to 461 in 2019

- $150,000-$200,000 sales fell to 323 (-19%) sales compared to 400 in 2019

- $200,000-$250,000 sales rose to 554 (9%) sales compared to 509 in 2019

- $250,000-$300,000 sales rose to 417 (53%) compared to 273 in 2019

- $300,000-$350,000 sales rose to 272 (29%) compared to 211 in 2019

- Over $350,000 sales rose to 619 (67%) compared to 370 in 2019

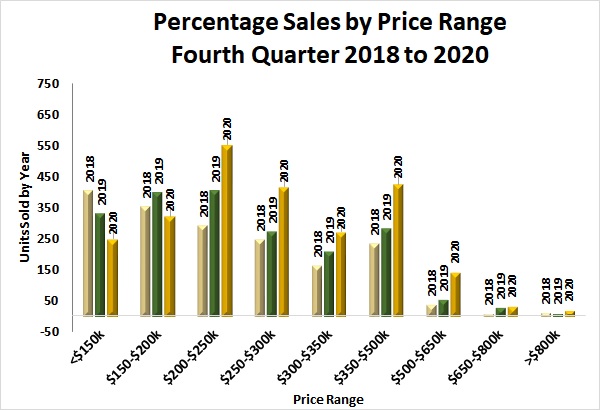

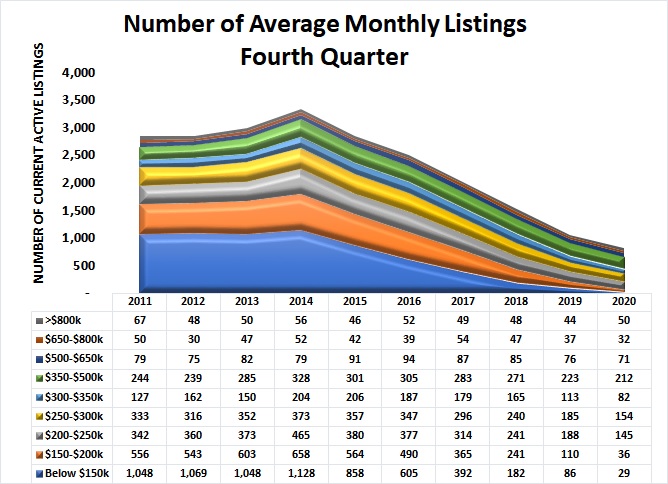

Inventory Price Band: Less than $150,000 fell to 29 (-66%) homes vs. 86 in 2019

- $150,000-$200,000 fell to 36 (-67%) homes vs. 110 in 2019

- $200,000-$250,000 fell to 145 (-23% homes vs. 188 in 2019

- $250,000-$300,000 fell to 154 (-17%) homes vs. 185 in 2019

- $300,000-$350,000 fell to 82 (-27%) homes vs. 113 in 2019